For some people, “budget” has become a four-letter word (I know it’s six letters, stick with me here). But it doesn’t have to be! Budgeting is simply deciding, intentionally, how to spend your hard-earned money. Why is this important? Because if you don’t have a plan for your money, it can easily slip through your fingers. You’ll look back at the end of the month and have no idea where it went and have nothing to show for it.

One big key to budgeting is to plan out how you’re going to spend your money BEFORE you have it. For example, we’re currently at the end of July which means you should be working on your August budget now. Why? It’s like planning for a vacation.

Say you’re going to spend a week in Colorado (you definitely should, it’s beautiful here!). Would you wait until the day you’re supposed to leave to decide how you’re going to get there, where you’re going to stay, and what you’re going to do while you’re there? Of course not! You know ahead of time that you’ll be driving your van, so you have plenty of room for the kids and suitcases (God bless you for braving a road trip with kids), you’ll be staying with family for three nights in Denver where you’ll catch a Rockies game, spend a day at Elitch Gardens, and of course you’ll be having dinner one night at Casa Bonita. Then, you’ll be heading to Glenwood Springs for a few days to stay at the Hotel Colorado because by this point, you’re going to need to relax in the hot springs! (Make sure to take in the vaudeville show while you’re there too.)

You plan your trip weeks, if not months, ahead of time so that you can have the best time and take advantage of every minute of vacation time you have. What if you put that much intentionality into creating a budget? You can, and I would argue, you should.

Never budgeted before? No problem, I’ll walk you through it. Just like planning ahead for your trip, you’re going to break down the what, when, and how much for the next month.

What – What income do you have coming in and what expenses do you having going out?

When – When does that income come in and when are your expenses due?

How Much – How much income do you have coming in and how much are your expenses?

Let’s start with calculating your total monthly income. Get a budgeting app, spreadsheet, or notebook (my preference) and list your income at the top. Income is any and all money that you expect to earn each month including wages, salary, commissions, bonuses, birthday money from grandma, etc. Next, write down when you get paid (weekly, bi-weekly, monthly, etc.). Lastly, how much do you get each pay period?

Now let’s move onto your expenses. This is any and all money you expect to pay the next month (mortgage/rent, utilities, car payment, student loans, coffee fund, etc.). Take into account what the next month is and think of any “extra” items you might have. For example, if you’re working on your August budget, don’t forget about school starting (let’s be honest, no parents will forget this, we’ve been counting down the days), and you’ll likely need to buy school supplies, fees, and clothes. Budget for those! Write down how much each expense is and when it’s due.

Now comes the fun part (speaking like the true nerd I am). We’re doing what’s called a zero-based budget. This simply means that after we’ve budgeted for everything, we’ll then calculate our total income minus our total expenses, and we should be left with zero. Every dollar we bring in needs to have a place to go. If your budget balances on your first try, congratulations, you’re a budget ninja! If you’re like the rest of us, you’ll likely have some adjusting to do. We’re avoiding going into debt, so the goal is to not have your expenses exceed your income.

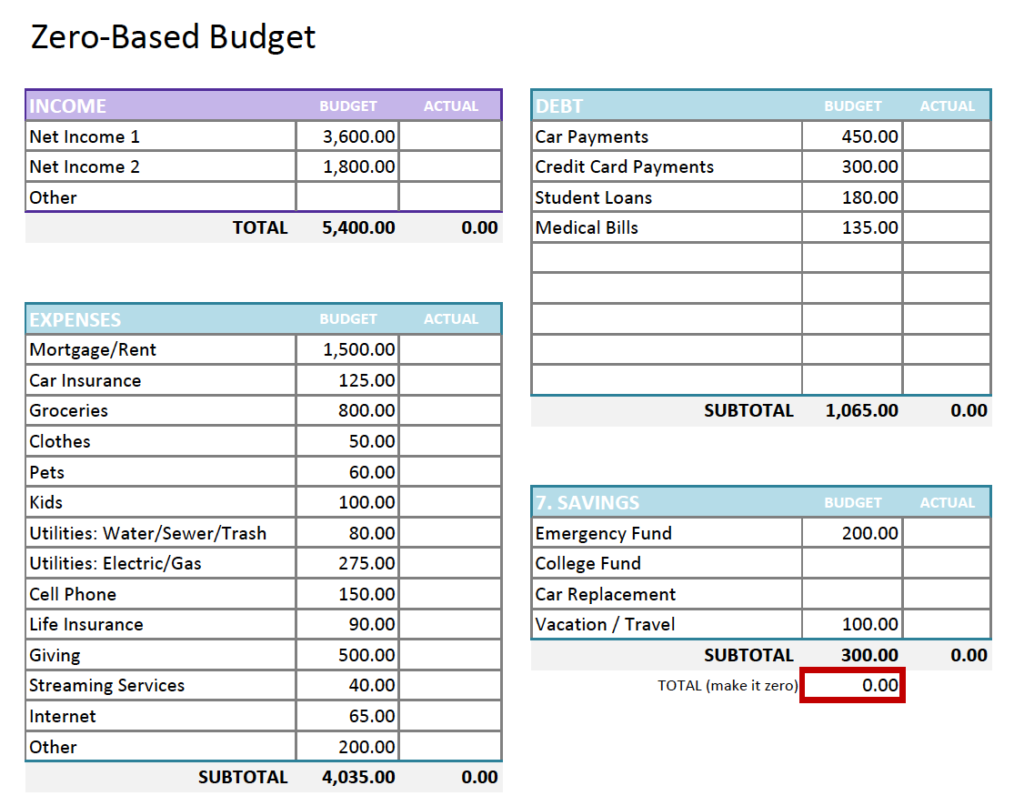

See the sample budget below.

I know depending on where you live some of these numbers might seem too high, too low, or just right, but please remember this is just an example. Everybody’s financial situation will look different, and even your own budget will usually be at least slightly different each month. Remember how we talked about school starting next month? You would need to add a line item for that. We’ll cover unplanned expenses in another post but do your best to think ahead and anticipate what you might have coming up.

Once your budget is balanced, take a look at when you get paid and when your expenses are due and plan accordingly. If your mortgage payment isn’t due until the end of the month but your electricity bill is due on the 5th, pay the electricity first so you don’t get late fees. It might be helpful to get a calendar or use the one on your phone to plan everything out, especially if you’re new to budgeting.

Lastly, give yourself some grace! If you’ve never budgeted before, it’s probably going to take longer than you think to do your first one and you’re going to make mistakes. Don’t let this discourage you though! On average, it takes about three months to figure out your numbers. (Turns out budgeting $200 a month for groceries for a family of four might not be realistic.) The most important point is that you’re actually doing the damn thing! You’re so much further ahead than you were last month because you’re being intentional. Keep going and don’t give up. I believe in you!

Reach out with any questions and until next time, spend with purpose and save with pride!